Rigid Trucks & Body Trucks Insurance

Insurance for rigid body trucks, curtainsiders, flat decks, and crane trucks used for urban and regional delivery.

⚠️ Key Risks

- •Urban delivery incidents with cyclists and pedestrians

- •Loading dock accidents and reversing damage

- •Theft of vehicle and load overnight

- •Kerbside impact damaging body or crane

- •Driver fatigue on early morning runs

✓ Coverage Checklist

- ✓Comprehensive motor vehicle cover

- ✓Goods in transit cover

- ✓Public liability

- ✓Body and equipment cover

- ✓Downtime and loss of use

- ✓Personal accident for driver

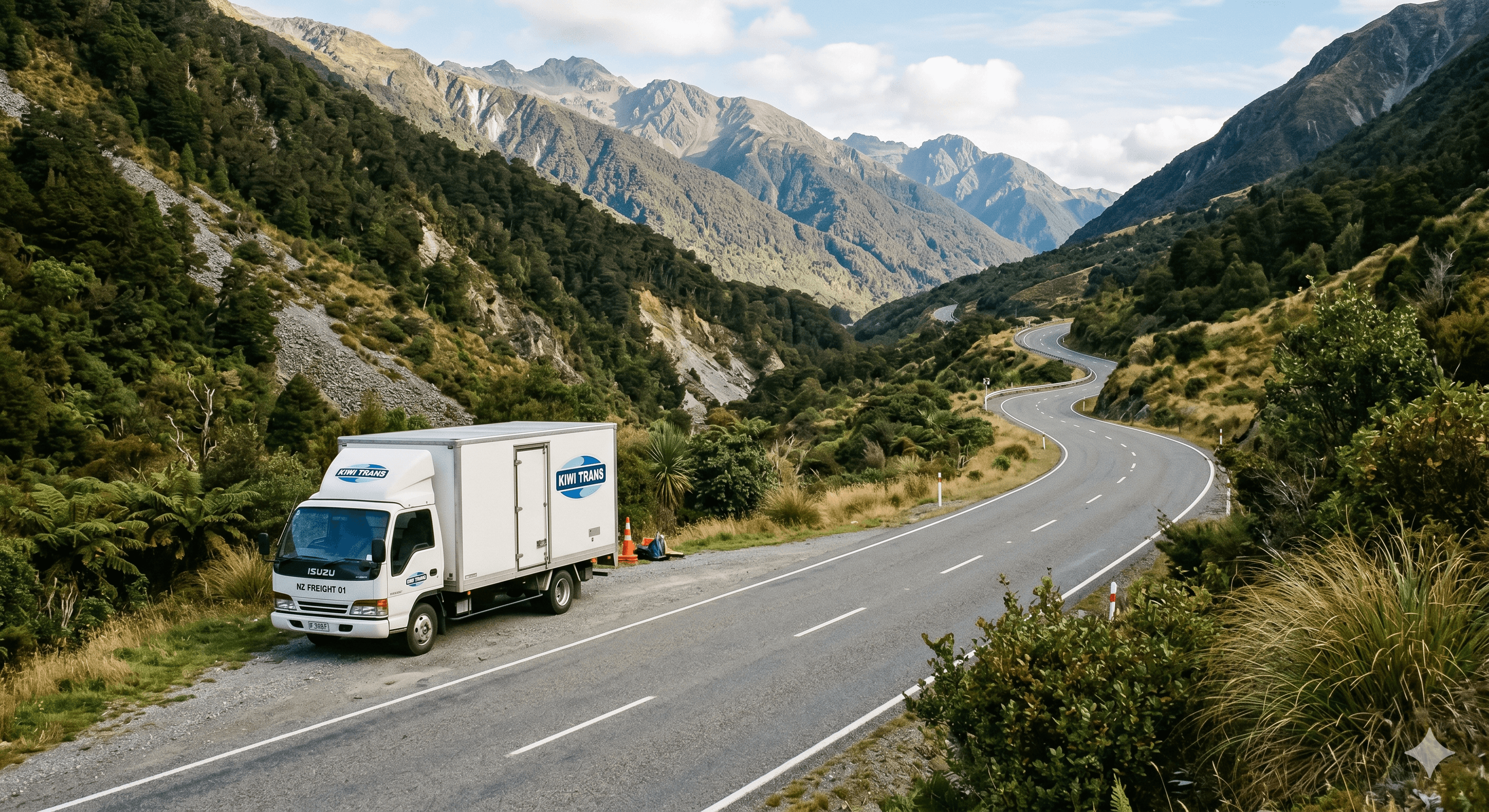

Rigid trucks are the workhorses of urban and regional distribution. Whether you are running a curtainsider delivering building supplies across Auckland, a flat-deck moving machinery to the Waikato, a crane truck servicing the Wellington CBD, or a refrigerated rigid supplying supermarkets on the Kapiti Coast, the insurance requirements are specific and non-negotiable. These vehicles operate in the most congested, high-frequency-incident environments of any heavy vehicle category — and the coverage must reflect that reality.

Rigid trucks — also called body trucks or single-drive trucks — sit in the 8 to 18 tonne GVM range. They are more manoeuvrable than artics but still large enough to cause serious damage in an accident, and valuable enough that an uninsured write-off could end a small operator's business overnight. The coverage structure must address the vehicle itself, all fitted equipment, the cargo, and the third-party risks created in the environments where these trucks operate every day.

GVM Classes and Why They Matter for Insurance Rating

Rigid trucks are categorised by GVM (gross vehicle mass) into distinct classes. This classification affects licensing requirements under the Land Transport Act 1998, RUC (road user charges) rates, COF (Certificate of Fitness) intervals, and insurance premium rating.

An 8-tonne GVM rigid is a common delivery vehicle — smaller curtainsiders, refrigerated rigids, and service vehicles operating in tight urban environments and residential streets. Their exposure profile is dominated by low-speed manoeuvring incidents, cyclist and pedestrian proximity risk, and loading dock incidents.

A 12-tonne GVM rigid covers the mid-range — larger flat decks, curtainsiders, and specialist body vehicles carrying heavier loads on construction sites and commercial deliveries. Off-road and site-access exposures become significant at this weight class.

Ready to get specialist cover?

Connect with a specialist broker — response within 24 hours.

An 18-tonne GVM rigid is at the upper end — heavy platform trucks, large crane trucks, and specialist body vehicles approaching the capacity of smaller artic combinations. Insurance reflects both the higher vehicle value and the significant third-party damage potential of these units.

[Waka Kotahi NZTA](https://transport.govt.nz) sets vehicle licensing requirements under the Land Transport Act 1998. Your RUC classification, COF regime, and operator licence conditions all affect your legal operating status — and an insurer who discovers your vehicle was operating outside its licence conditions at the time of a claim has grounds to decline cover. A specialist broker confirms that your policy aligns with your NZTA compliance status from day one.

Urban Delivery — The High-Frequency Risk Environment

City driving creates a fundamentally different risk profile from highway haulage. Stop-start traffic on Auckland's Southwestern Motorway, reversing into tight loading bays in Wellington's Customhouse Quay precinct, navigating Christchurch's post-rebuild construction zones on SH73, cyclists filtering past stationary delivery vehicles on Symonds Street — rigid truck operators face a higher frequency of small incidents than highway operators, even if the severity of individual events is lower.

Low-speed backing incidents are the single most common claim type. A moment of inattention reversing from a Countdown or Pak'nSave loading dock, a blind spot created by a curtainsider body, a missed spotter signal on a narrow site — and you have collected a bollard, a barrier, dock infrastructure, or a cyclist. Comprehensive cover with appropriate excess levels is essential. Some operators use dashcam and reversing camera footage to defend against spurious third-party claims — this equipment costs less than one claim excess.

Loading dock liability extends beyond the vehicle. If a driver damages dock infrastructure — dock levellers, bay doors, automatic barriers, or shelving racking — that damage may not be covered by the motor vehicle policy at all. A public liability extension that specifically covers loading and unloading operations is necessary. Confirm with your broker exactly how your policy responds to damage caused during unloading, as distinct from damage caused by a vehicle collision.

Ready to get specialist cover?

Connect with a specialist broker — response within 24 hours.

Overnight theft is a growing risk for rigid trucks parked in urban locations. The vehicle itself, fitted equipment (tail lifts, HIAB cranes, refrigeration units), and the cargo are all targets. If your truck parks loaded overnight in Auckland, Hamilton, or Wellington on a regular basis, your insurer will want to know what security measures are in place: GPS tracking, cab immobilisers, load compartment alarms, and secure parking facilities. Theft from unattended vehicles is frequently subject to additional policy conditions — read these carefully and comply with them.

Body and Equipment Cover — The Detail That Matters

Many rigid trucks carry substantial additional equipment. HIAB loader cranes, tail lifts, compactors, refrigeration units, tanker bodies, flatbed tie-down systems, and specialist measurement or service equipment can add $20,000 to $120,000 to the vehicle's total replacement cost. Every piece of this equipment must be specifically noted in the policy schedule with its own value.

Operators who discover at claim time that a fitted crane or refrigeration unit was only partially covered — grouped under a generic "accessories" sub-limit of $5,000 when the actual replacement cost is $70,000 — face a significant and avoidable shortfall. Your broker should itemise all fitted equipment: make, model, purchase date, and current replacement cost. Review this list at every renewal and notify your broker immediately when new equipment is added. An unnotified addition is an uninsured addition.

The HIAB crane deserves particular attention. A mid-range HIAB loader crane — an HIAB X-HiDuo 138 or equivalent — costs $80,000 to $150,000 new. If the crane is damaged in a road accident, the motor vehicle section responds. If the crane fails during a lifting operation and drops a load, lifting operations liability responds — which is a separate cover that must be specifically arranged. A broker who does not ask about your HIAB's lifting use as well as its road use has left a gap in your programme.

Goods in Transit vs Carriers Liability — Knowing the Difference

These two covers address different exposures, and the confusion between them is one of the most common mistakes rigid truck operators make.

Ready to get specialist cover?

Connect with a specialist broker — response within 24 hours.

Goods in transit is property cover. It pays for physical loss or damage to goods — whether they belong to you or to a client. If you are a retailer or manufacturer running your own delivery truck carrying your own stock, goods in transit is the right product.

Carriers liability is liability cover. It pays your legal liability to the goods owner under the Contract and Commercial Law Act 2017 (CCLA) when you carry third-party freight for reward. If you are a transport operator carrying clients' goods, carriers liability is non-negotiable. It is what stands between you and a freight owner's full-value claim for goods lost, damaged, or stolen in your care.

For operators who carry both their own goods and clients' freight — a common situation for trade suppliers running their own delivery fleet and also doing local haulage for others — both covers may be needed simultaneously. A specialist broker structures both correctly and ensures the combined limits reflect your actual cargo exposure.

Multi-Driver and Relief Driver Policy Structure

Rigid truck operations often use multiple drivers across shifts, routes, and days. A regular driver plus a relief driver, a casual weekend driver, or a subcontractor filling in during busy periods — all are common arrangements. Some policies restrict cover to specifically named drivers, which creates an uncovered gap the moment a non-listed driver is behind the wheel.

An open-driver or any-qualified-driver policy covers any driver who holds the appropriate class licence, without requiring them to be individually named. The tradeoff is a modest premium loading over a named-driver policy — but the alternative, an uncovered claim because a relief driver was at the wheel, is a catastrophically worse outcome. If your operation uses relief drivers at any point, an open-driver policy is the only appropriate structure.

Ready to get specialist cover?

Connect with a specialist broker — response within 24 hours.

Refrigerated Rigid Variants and the Food Act

A refrigerated rigid — typically 8 to 14 tonnes GVM with a Carrier Transicold or Thermo King unit mounted behind the cab — is one of the most complex rigid truck risks to insure correctly. Three elements must be covered explicitly: the refrigeration unit as a declared item with its own value; cargo spoilage cover responding to temperature excursion caused by equipment failure; and carriers liability sized to the maximum value of chilled or frozen product you carry on any single run.

The NZ Food Act 2014 places obligations on food businesses in temperature-controlled supply chains. A cargo spoilage claim involving a regulatory breach — food carried at incorrect temperatures without temperature log records — may face coverage challenges at claim time. Continuous temperature logging with a calibrated data recorder is both a Food Act compliance tool and the evidence that supports your insurance claim. Implement it, maintain it, and keep the records.

Employer Obligations and Statutory Liability

If you employ drivers, the Health and Safety at Work Act 2015 places obligations on you as a PCBU to manage the risks your drivers face: heavy vehicle collision risk, fatigue, manual handling during loading and unloading, and the specific hazards of urban delivery environments. [WorkSafe NZ](https://worksafe.govt.nz) enforces these obligations and investigates serious incidents involving rigid truck operators.

Employers liability cover pays defence costs and any awards if an employee makes a successful claim against you for a workplace injury beyond what ACC covers. Statutory liability cover pays defence costs and penalties if WorkSafe prosecutes your business for an HSW Act breach. Both are relevant to any operator employing drivers, and both are typically available as extensions to your motor vehicle policy through a specialist HGV broker.

Agreed Value and the Body Truck Market

Rigid trucks hold their value differently from artic prime movers. Specialist body configurations — purpose-built refrigerated bodies, compactor bodies, crane truck configurations — add value that is not captured in standard market valuation guides. A rigid truck with a custom refrigerated body and tail lift may have a total replacement cost of $180,000 when the standard second-hand market price for the chassis alone is $70,000. Insuring at the chassis-only value leaves a $110,000 gap — almost certainly more than the operator can absorb.

Ready to get specialist cover?

Connect with a specialist broker — response within 24 hours.

Agreed value policies for rigid trucks should include a separate agreed value for the body and all fitted equipment, reviewed annually. If a body was custom-built — a specialist food service refrigerated body, a purpose-designed compactor, or a crane truck configuration — obtain a current replacement quotation from the body builder at renewal and use that figure as the basis for the agreed value. Do not rely on what you paid for the body three years ago; build costs have changed significantly.

RUC and Compliance Cost Exposure

Road user charges (RUC) compliance is a significant operational obligation for rigid truck operators. Under the Land Transport Act 1998 and the Road User Charges Act 2012, operators must hold valid RUC licences for the distance and vehicle weight class operated. NZTA RUC enforcement officers conduct roadside checks, and non-compliance — particularly a vehicle operated without a current RUC licence — can result in penalties, vehicle prohibition, and investigation of the operator's broader compliance record.

A RUC prosecution does not trigger your motor vehicle insurance — it is a regulatory matter. Statutory liability cover, however, provides defence cost support and penalty cover if a RUC or other regulatory prosecution follows an incident. This is a relatively low-cost extension with meaningful value for operators running high-distance rigid truck operations across multiple routes and regions.

To connect with a specialist broker for rigid truck insurance, complete the quote request on this page and expect a response within 24 hours.

Frequently Asked Questions

Is a tail lift or HIAB crane covered under my truck policy?

Only if you declare it. Fitted body equipment must be specifically noted in your policy schedule. Always provide your broker with a full list of fitted equipment including manufacturer, model, and current replacement cost.

What is the difference between goods in transit and carriers liability?

Goods in transit covers physical loss or damage to freight. Carriers liability covers your legal liability to the freight owner under your carriage contract. You may need both — speak to a specialist broker to structure your cover correctly.

Do I need public liability as well as vehicle insurance?

Yes. Vehicle insurance covers damage to your truck. Public liability covers injury or property damage to third parties that isn't directly caused by a vehicle collision — for example, a load that falls during unloading, or damage caused on a client's loading dock. It's a separate but equally important cover.

What GVM triggers a requirement for a specialist HGV policy?

Technically any vehicle over 3.5 tonnes GVM is a heavy vehicle under the Land Transport Act 1998, but insurers typically apply specialist HGV rating and policy terms from around 8 tonnes GVM. Below that, commercial vehicle policies often suffice. Your broker will advise on the appropriate product for your specific vehicle.

Get a Rigid Trucks Quote

Specialist broker response within 24 hours