Livestock & Agriculture Insurance

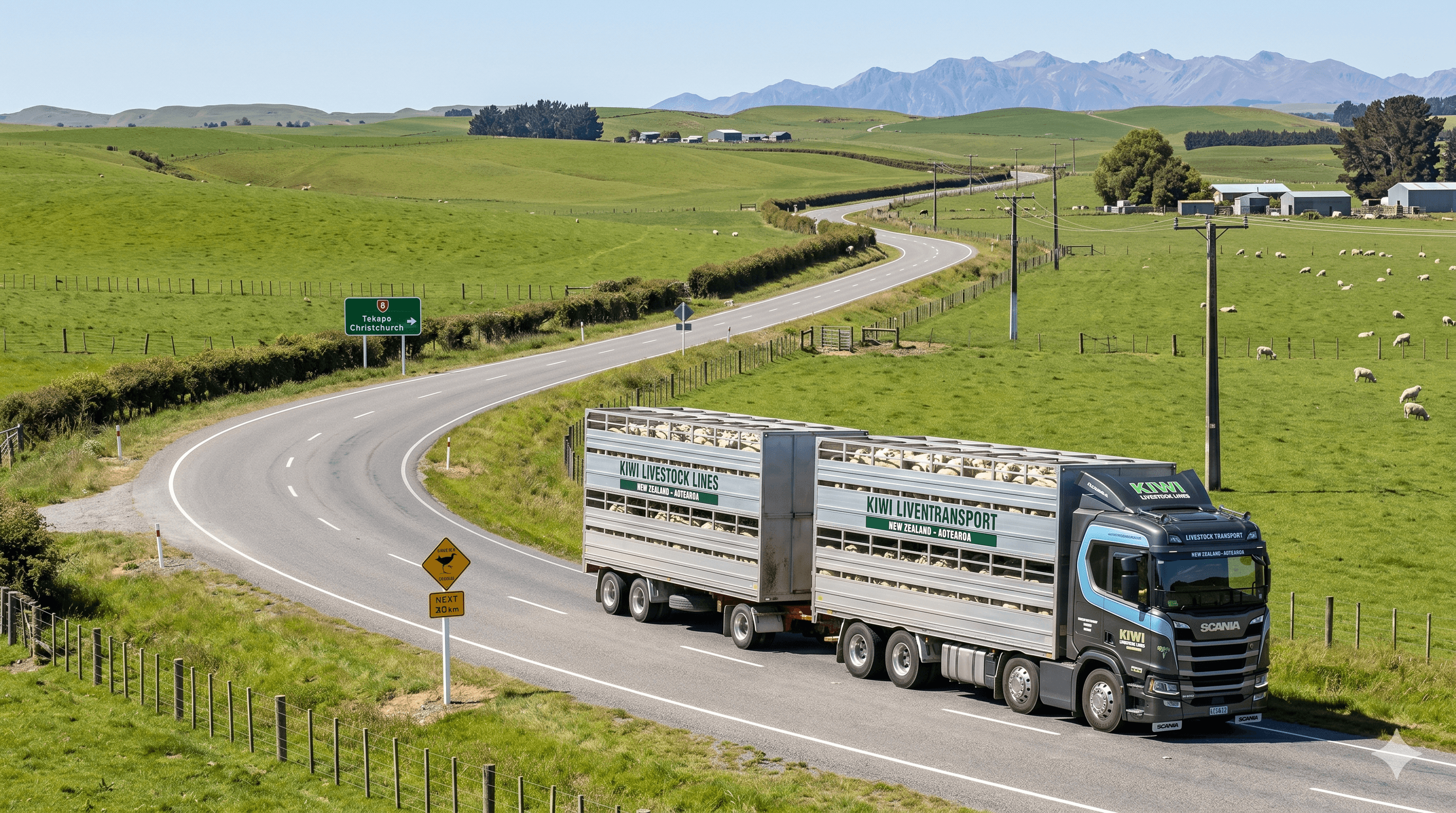

Livestock carriers, stock trucks, and agricultural transport operators moving cattle, sheep, deer, pigs, and horses between farms, saleyards, and processing plants.

Coverage Needs for This Sector

Vehicle Types in This Sector

Livestock transport is one of the oldest and most important sectors of the rural economy. Moving cattle, sheep, deer, pigs, and horses between farms, saleyards, processing plants, and export facilities requires specialist vehicles, experienced drivers, and insurance that understands the unique risks of carrying live cargo — cargo that can die, escape, injure people, and generate biosecurity liability that no standard freight policy addresses.

The Livestock Production Regions

The geography of livestock transport follows the geography of livestock production:

Southland and Otago are the primary sheep and beef cattle regions. The movement of store cattle between summer and winter grazing properties, the autumn run of finished cattle and lambs to works at Finegand (Balclutha), Alliance Group (Lorneville, Invercargill), and Silver Fern Farms facilities throughout the region creates sustained high-volume stock movement. Winter road conditions — ice, snow, high country access — add operational risk.

Canterbury is the largest mixed farming region — sheep, beef, dairy, and increasingly deer. The Canterbury Plains and hill country generate substantial stock movement, with saleyards at Temuka (South Canterbury) and Leeston serving as key aggregation points. Road conditions on the braided river plains and the foothills access routes are variable and weather-sensitive.

Waikato is the primary dairy region, with dairy support livestock (young stock, replacements, culls) generating significant transport demand alongside the dairy collection network. The Feilding Saleyard in the Manawatu is one of the largest livestock trading centres in the Southern Hemisphere — saleyard days here involve hundreds of vehicles and tens of thousands of animals in a compressed timeframe.

Ready to get specialist cover?

Connect with a specialist broker — response within 24 hours.

Northland has significant beef cattle production on hill country farms with limited processing capacity locally — cattle regularly travel south to Waikato and beyond for finishing and processing.

The Animal Welfare Act 1999 — Your Legal Obligations

The Animal Welfare Act 1999 (AWA) imposes legal obligations on livestock carriers for the animals in their care. These obligations are not aspirational — they are enforceable, and a carrier who breaches them and animals die as a result may find their insurance claim affected.

[MPI](https://mpi.govt.nz) administers the Code of Welfare for Land Transport of Livestock, which sets minimum standards for:

- Journey time limits by species and class of stock (for example, sheep: maximum 28 hours without off-loading for rest, feed, and water) - Stocking densities — maximum number of animals per square metre of deck space by species and size - Feed and water access — requirements for rest stops on long journeys - Fitness to travel — obligations to refuse to load animals that are not fit for transport (visibly lame, heavily pregnant animals within certain periods of due date, animals with open wounds) - Driver competency — requiring drivers to be able to assess animal welfare and respond to welfare emergencies

A carrier who loads animals that are unfit to travel, exceeds journey time limits, or operates at excessive stocking densities, and animals die or are injured as a result, faces a potential AWA prosecution alongside an insurance claim that may be challenged on the grounds that the loss was caused by the carrier's regulatory breach.

Ready to get specialist cover?

Connect with a specialist broker — response within 24 hours.

Livestock Mortality Extension — Why It Matters

Standard carriers liability policies cover physical goods — they are designed for crates, pallets, and packages. They do not automatically cover animal mortality during transit. The death of animals during transport requires a specific livestock mortality extension that explicitly covers financial losses arising from animals dying while in your care and custody.

The value of animals in transit varies significantly:

- Store lambs at saleyards: $80–$180 each. A deck of 400 lambs is $32,000–$72,000 in cargo value. - Finished beef cattle: $1,500–$3,500 each. A load of 30 cattle is $45,000–$105,000. - Stud bulls: $10,000–$100,000+ individually. A single stud bull transport movement may require specific individual cover. - Thoroughbred horses: $20,000–$500,000+. Horse transport requires specialist treatment (see below).

When you are carrying a mixed saleyard load — 200 cattle from five different vendors — the total cargo value can easily reach $400,000–$600,000. Your livestock mortality extension must be sized accordingly.

Saleyards Routes — Feilding, Stortford Lodge, Temuka

Saleyard day operations create specific risk profiles. The major saleyards — Feilding (Manawatu), Stortford Lodge (Hastings), and Temuka (South Canterbury) — process thousands of animals on trading days. Carriers working these saleyards:

Ready to get specialist cover?

Connect with a specialist broker — response within 24 hours.

- Complete multiple loads in a single day (elevated driver fatigue risk) - Load unfamiliar animals from multiple vendors (unknown temperament, potential welfare status variation) - Operate in crowded yard environments with multiple other vehicles, handlers, and animals present - Work under time pressure of saleyard trading sessions and processing schedules

Incidents at saleyards — loading ramp injuries (to animals and handlers), vehicle damage in congested yards, animals escaping — are disproportionately common on high-volume trading days. Your insurance needs to cover the full range of your operating pattern, including saleyard days.

Biohazard Cleaning and Biosecurity Liability

The biosecurity risk of livestock transport is serious. The movement of disease between properties — via animals, vehicle surfaces, effluent, and soil — is regulated under the Biosecurity Act 1993 administered by [MPI](https://mpi.govt.nz). Specific biosecurity risks include:

Mycoplasma bovis (M. bovis): An ongoing biosecurity challenge in the cattle herd. A carrier who transported infected cattle and failed to clean and disinfect their vehicle between movements could potentially contribute to disease spread — and face civil liability from affected farmers and potentially regulatory action under the Biosecurity Act.

Effluent management: Livestock trucks generate effluent during transit. Effluent spillage on public roads is both an environmental issue and a biosecurity risk. Carriers have obligations around effluent containment and must use designated effluent disposal stations. Biohazard cleaning after livestock transport is a significant cost — specialist cleaning is required before vehicles can move between properties under biosecurity protocols.

Ready to get specialist cover?

Connect with a specialist broker — response within 24 hours.

Insurance for biohazard cleaning costs and biosecurity liability (liability to third parties for disease spread caused by your vehicle) requires specific extension. Standard public liability does not automatically cover disease transmission liability.

Seasonal Risk Peaks

Livestock transport demand is highly seasonal, with specific peak risk periods:

Spring lamb: September–November. Large volumes of newborn and young lambs moving from lambing properties to hogget finishing, creating specific welfare challenges (cold stress, hypothermia risk in transit).

Autumn cattle: March–May. The major autumn cattle movement from summer hill country grazing to winter paddocks and works. High volume, high animal values, time pressure from weather and ground conditions.

Summer dry stock: December–February. Drought periods trigger emergency stock movements — destocking decisions made quickly under stress create elevated risk of welfare incidents and transport under suboptimal conditions.

Ready to get specialist cover?

Connect with a specialist broker — response within 24 hours.

Understanding your seasonal exposure pattern allows your broker to structure cover — and identify whether specific extensions (increased limits during peak periods, for example) are appropriate.

Road Conditions and Rural Access

Livestock carriers operate on some of the most challenging road surfaces in the country — unsealed rural roads, single-lane bridges, flooded river crossings during spring, and icy high country access routes in winter. These conditions create a vehicle damage profile that is different from highway operations: undercarriage damage from unsealed roads, body damage from narrow gates and tight yards, and rollover risk on steep farm tracks.

Make sure your comprehensive motor vehicle cover explicitly covers the full range of roads you operate on — including private farm access roads, unsealed forestry access, and river crossing areas. Some policies restrict cover to gazetted public roads; if your routes include private access, that restriction must be addressed.

Agreed value is particularly critical for livestock carrier vehicles, which often carry significant body value in addition to chassis value — specialist multi-deck livestock bodies cost $60,000–$120,000 to replace and may not be captured accurately by standard vehicle valuation approaches.

Fodder and Silage Haulage

Many livestock carriers also haul fodder and silage during drought periods — carrying hay, silage, and supplement from areas of surplus to drought-affected farms. This secondary cargo type has different insurance characteristics from live animal transport:

Ready to get specialist cover?

Connect with a specialist broker — response within 24 hours.

- Carriers liability (not livestock mortality) is the relevant cover - Load security risk differs from livestock decks (bales can shift, silage wrap can fail) - The contractual relationship with the farmer may differ from the standard livestock haulage arrangement

Disclose fodder haulage to your broker and confirm that your carriers liability cover applies to this cargo type.

Linking Animal Welfare and Insurance

Carriers who invest in driver training for animal handling — loading, journey monitoring, recognising distress — have lower mortality claims and better insurance outcomes. The New Zealand Veterinary Association and [MPI](https://mpi.govt.nz) provide guidance on animal handling best practice. Insurers who see consistent low-mortality claims history offer better terms at renewal.

The connection between animal welfare compliance and insurance is direct: a claim that arises from a documented animal welfare breach (journey time exceeded, stocking density too high) gives the insurer grounds to challenge the claim or reduce the settlement. Good welfare practice is not just ethically required — it is a financial protection.

Document your compliance: journey times, loading densities, rest stops, and driver certification records. If a mortality claim arises, this documentation demonstrates to the insurer that the loss was not caused by a welfare breach within your control. Without documentation, you cannot make this case.

Ready to get specialist cover?

Connect with a specialist broker — response within 24 hours.

Industry Bodies & Associations

Represents farmers and rural businesses across all commodity sectors.

Covers livestock transport sector including saleyards and stock movement.

Frequently Asked Questions

What happens if animals escape during loading and cause a road accident?

This is a public liability claim (injury or damage caused by escaped animals) and potentially a motor vehicle claim (if the vehicle is involved in the incident). Both covers should respond. Make sure your public liability limit is sufficient for the potential injury liability from escaped stock on a public road.

Do I need a specific policy for horse transport?

Commercial horse transport (carrying other people's horses for payment) typically requires a specific livestock carrier policy with an explicit horse transport endorsement. Standard HGV policies may not include cover for equine cargo — and the animal values involved make the distinction important.

Get a Livestock & Agriculture Quote

Specialist broker response within 24 hours

Sector-specialist brokers

Compare the brokers who specialise in livestock & agriculture insurance programmes.

Compare Brokers